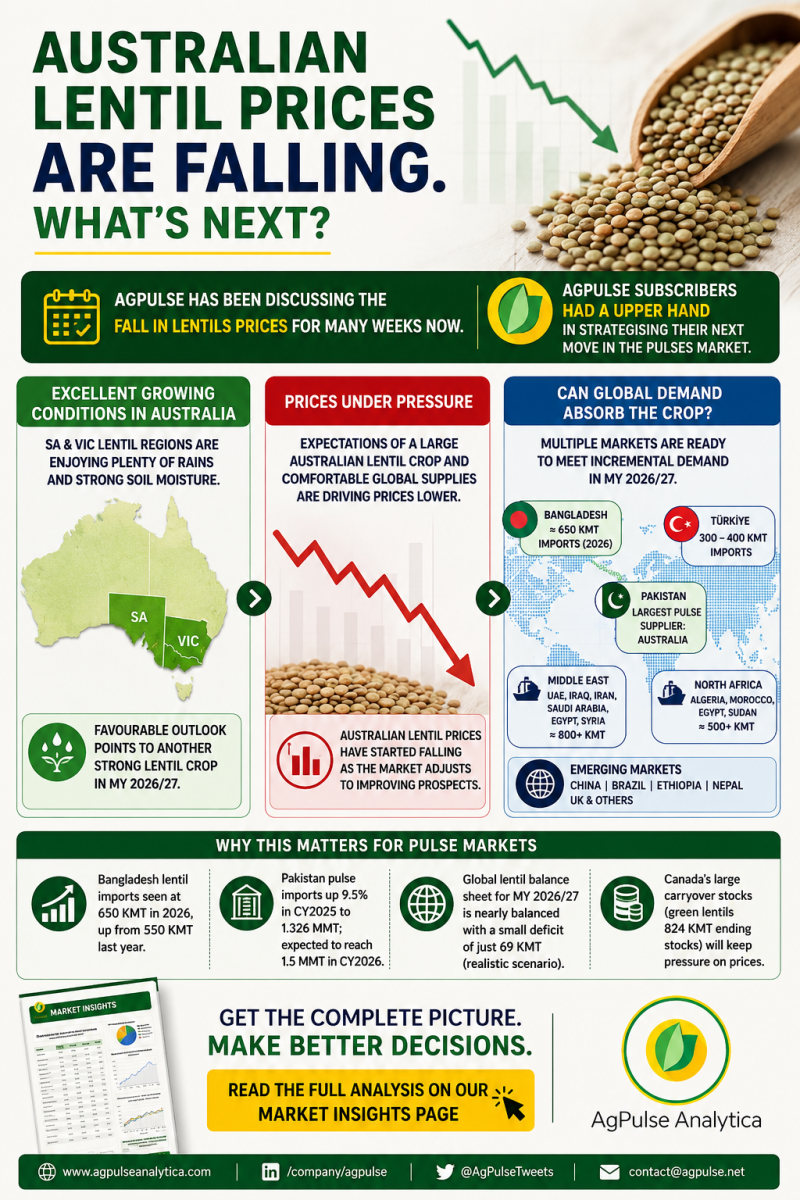

Australian Lentil Prices Are Falling. What Next?

02 June, 2026

Admin

Based on the numbers in our May Pulses Monthly sheet and the Australian weather analysis from the weekly reports, the market is currently underestimating how much of the potential Australian lentil crop can actually be absorbed.

The key is that traders are looking at the production side (excellent SA and VIC conditions), while the monthly sheet reveals a surprisingly healthy demand side.

If Australia achieves the realistic scenario of 1.6 MMT lentil production and exports 1.4 MMT, or even the optimistic scenario of 1.78 MMT production and 1.6 MMT exports, the question becomes: where does the extra volume go?

The first and most obvious destination remains the Indian subcontinent.

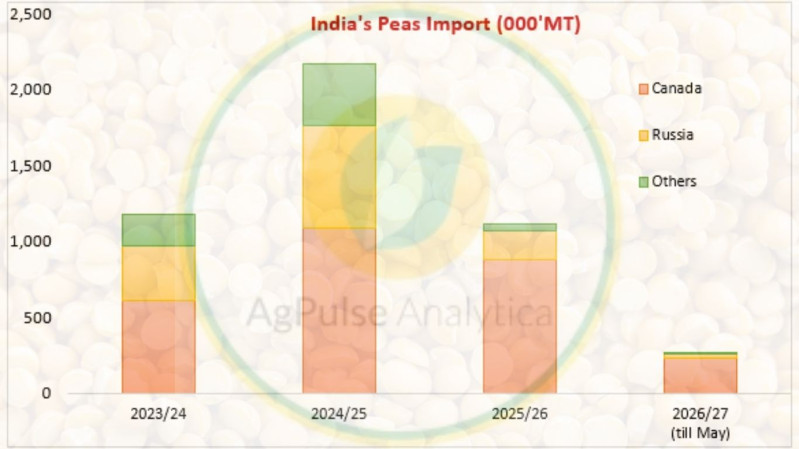

India's lentil imports are projected at 1.147 MMT in FY 2025/26 according to the weekly report, while South Asian pulse demand remains elevated due to tighter availability of competing pulses. Although the monthly sheet shows stronger focus on peas and chickpeas, the broader theme across all reports is that Indian pulse consumption remains robust.

The second market is Bangladesh, which may actually be one of the most important growth engines. The monthly sheet explicitly projects Bangladeshi lentil imports rising to 650 KMT in 2026, compared with 550 KMT last year, because Ramadan demand for both 2026 and 2027 will largely be supplied through imports during calendar year 2026. That is a very significant increase and Bangladesh traditionally favours red lentils.

The third market is Türkiye.

Many traders are focusing on the expected recovery in Turkish production and therefore assuming imports collapse. The monthly sheet does not support that view. While imports are expected to decline from the unusually high levels of the current year, Türkiye is still projected to import 350 KMT of lentils in the realistic scenario, with imports ranging from 300–400 KMT.

Furthermore, the May 25 weekly specifically states that Türkiye is likely to continue importing lentils in MY 2026/27 at a pace similar to the current year.

The fourth market is the Middle East.

The "Sundry Lentils Importers" table reveals a surprisingly large and growing import base. For 2026, AgPulse projects:

· UAE: 350 KMT

· Iraq: 160 KMT

· Egypt: 150 KMT

· Iran: 80 KMT

· Saudi Arabia: 70 KMT

· Syria: 22 KMT

Collectively, that is well over 800 KMT of annual demand from the Middle East alone.

The fifth market is North Africa.

The sheet projects:

· Algeria: 160 KMT

· Morocco: 70 KMT

· Sudan: 105 KMT

· Egypt: 150 KMT

North Africa therefore represents another demand pool approaching 500 KMT.

What we find particularly interesting are the emerging secondary markets.

The monthly sheet shows:

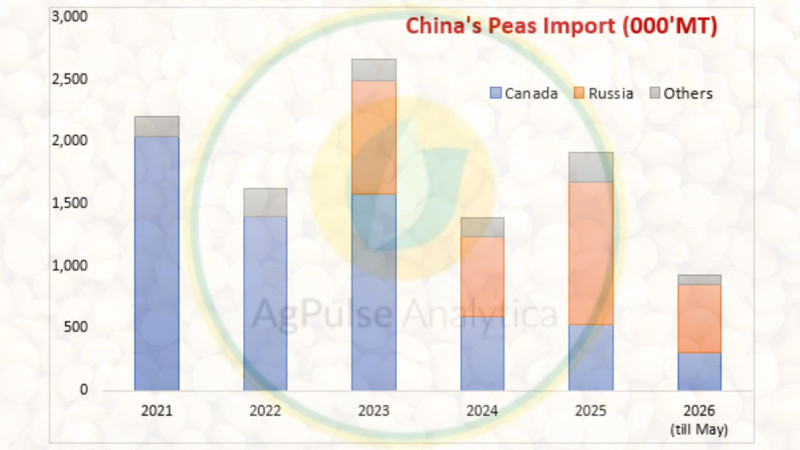

· China rising from 29 KMT to 38 KMT

· Brazil rising from 17 KMT to 25 KMT

· Ethiopia rising from 30 KMT to 55 KMT

· Nepal rising from 50 KMT to 75 KMT

· UK rising from 47 KMT to 52 KMT

None of these markets individually move prices, but collectively they represent incremental demand growth that wasn't present a few years ago.

The bigger issue may not be whether the world can absorb Australian lentils. The bigger issue may be whether the world can absorb Australian lentils plus Canadian carryout stocks simultaneously.

Our monthly sheet highlights that Canadian lentil stocks remain enormous. Green lentil ending stocks alone are projected at 824 KMT in the realistic scenario for 2026/27, after carrying 934 KMT into the season. The report explicitly states that even with a sharply smaller crop, farmers may have to carry stocks into 2027/28.

That is where the bearish pressure is coming from.

The global lentil balance sheet in the monthly sheet is not overwhelmingly bearish. In fact, AgPulse projects the 2026/27 world lentil balance sheet to be close to neutral, with a deficit of only 69 KMT in the realistic scenario.

So if Australia produces a large lentil crop, the market likely has enough demand growth from:

· Bangladesh (+100 KMT imports),

· Türkiye (still 300–400 KMT imports),

· Middle East demand,

· North Africa demand,

· Emerging Asian markets,

to absorb most of it.

The real risk to prices is not Australia alone. It is the combination of:

1. Another excellent Australian lentil crop,

2. Massive Canadian carryover stocks,

3. Recovery in Turkish production,

4. Lack of a major new demand shock.

That combination can keep prices under pressure even though global consumption itself appears healthy and continues to grow according to the monthly sheet. In other words, the demand side is not weak; it is simply struggling to outrun the accumulated inventories sitting in Canada and potentially building again in Australia.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us