Deep Dive: India’s 2027 Pulse Import Policy Extension

22 May, 2026

Admin

Why the Market Should View This as More Than a Short-Term Inflation Measure

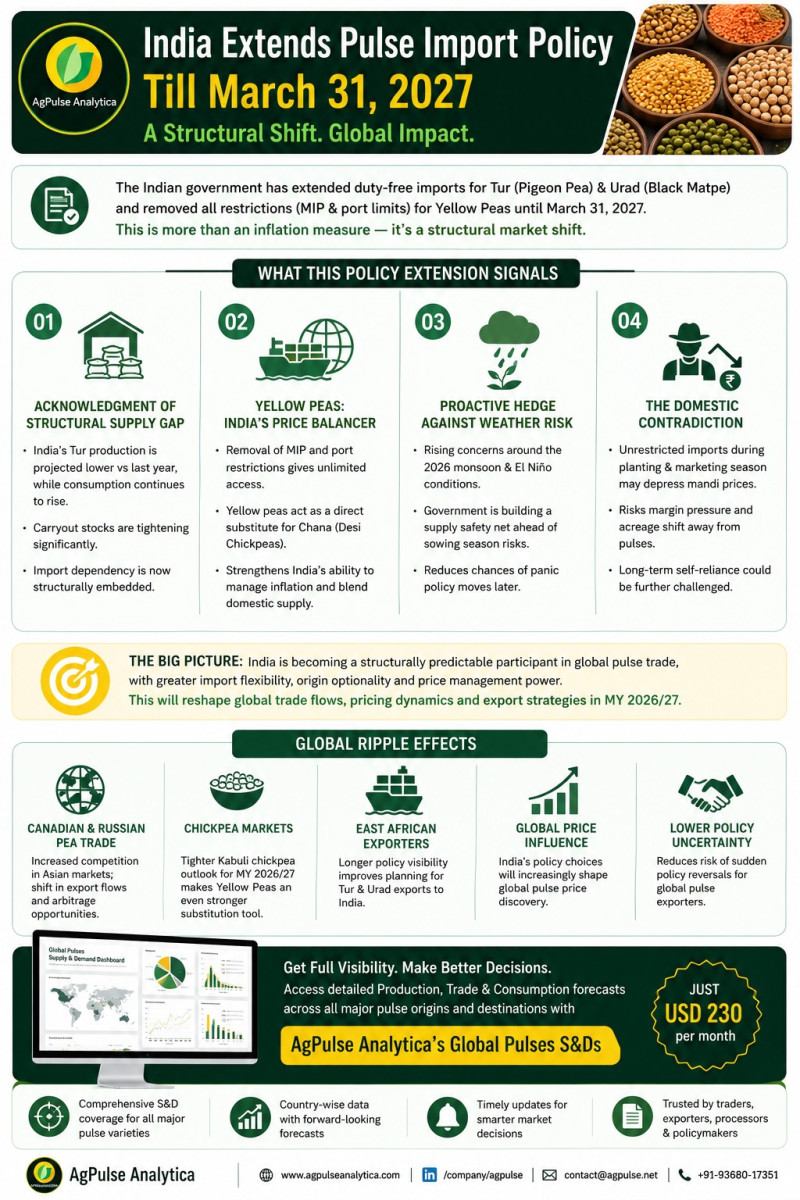

The Indian Ministry of Commerce and Industry, through the Directorate General of Foreign Trade (DGFT), has extended the duty-free import window for Tur (Pigeon Pea) and Urad (Black Matpe), alongside relaxed import conditions for Yellow Peas, until March 31, 2027.

At first glance, the move appears to be a straightforward food inflation management strategy. However, structurally, this policy extension signals something much larger:

????India is acknowledging that domestic pulse supply volatility remains too large to manage without aggressive integration into global supply chains.

For global pulse markets, this decision materially alters trade visibility for MY 2026/27.

1. Tur & Urad: India Is Signalling Structural Dependence

The extension of zero-duty imports for Tur and Urad effectively confirms that India’s domestic production recovery remains insufficient to create policy comfort.

AgPulse Analytica’s balance sheet projections indicate that Indian pigeon pea production for the current cycle remains below the previous year, while domestic consumption continues to expand. Simultaneously, carryout stocks are projected to tighten significantly versus last season, reducing the government’s flexibility in managing domestic supply shocks.

This is critical because India exhausted a substantial portion of the comfortable stock cushion accumulated during the aggressive import phase of FY25.

As a result:

For East African exporters such as Mozambique, Tanzania and Malawi, this creates a much longer visibility window for trade planning.

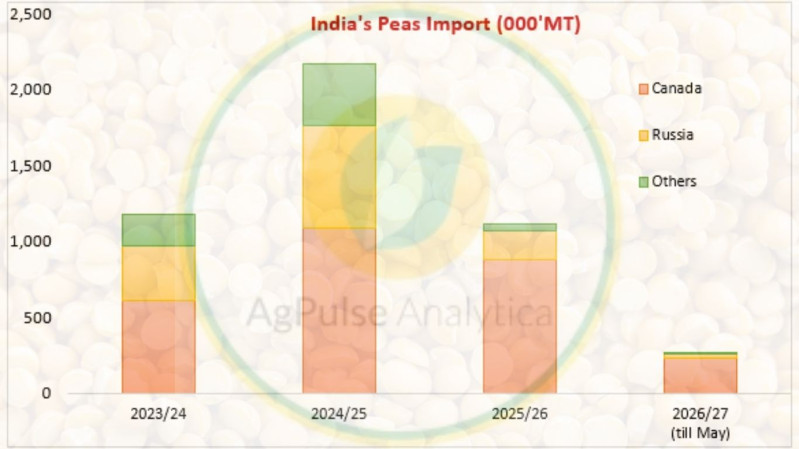

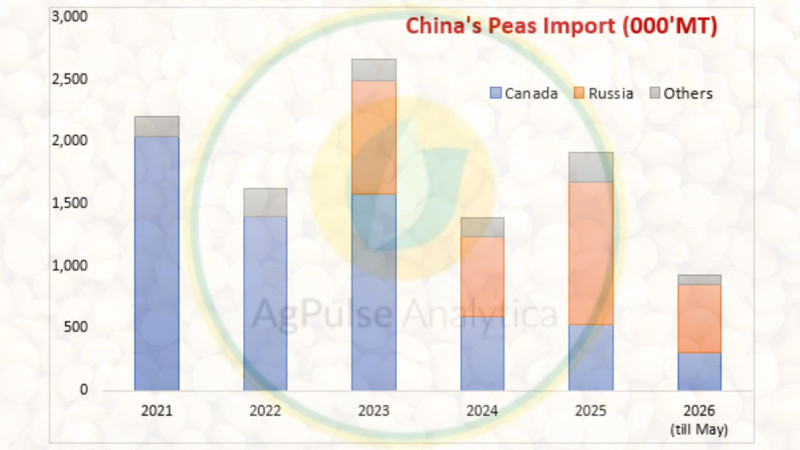

2. Yellow Peas: The Real Strategic Weapon

The most underappreciated component of the policy extension is the continuation of unrestricted Yellow Pea imports.

By removing both:

India has effectively converted Yellow Peas into a permanent price-balancing instrument for its domestic pulse economy.

This matters because Yellow Peas directly compete with Chana (Desi Chickpeas) in processing channels.

AgPulse Analytica’s global chickpea balance sheet projections suggest that after multiple surplus years, global Kabuli chickpea markets are beginning to tighten modestly in MY 2026/27, with world trade projected to soften versus the previous cycle while consumption continues expanding.

In such an environment, unrestricted Yellow Pea imports provide India with:

The impact extends beyond India.

This policy potentially reshapes:

3. India Is Quietly Pricing in Weather Risk

The timing of the extension is equally important.

The policy arrives amid increasing concerns regarding the 2026 monsoon cycle and elevated probability of weather irregularities linked to El Niño conditions.

AgPulse Analytica’s outlook notes that increasing climatic uncertainty could materially cloud production estimates for the upcoming Indian pigeon pea crop.

The government appears to be proactively constructing a supply safety net before the sowing season risk fully materializes.

This significantly reduces the probability of panic policy decisions later in the marketing year.

4. The Domestic Contradiction: Food Security vs Farmer Economics

While the policy improves consumer-side inflation stability, it simultaneously intensifies pressure on domestic pulse growers.

With unrestricted imports now overlapping the domestic planting and marketing cycle, local mandi prices could remain under sustained pressure.

This creates a classic macroeconomic conflict:

The risk is that persistently weak realizations may incentivize acreage migration toward crops with more stable returns, including oilseeds and cotton.

Ironically, this could deepen India’s long-term import dependence even further.

5. The Global Trade Implication

The extension effectively transforms India from a sporadic policy-driven importer into a more structurally predictable participant in global pulse trade.

For exporters, this reduces one of the largest historical uncertainties in the pulse market:

????sudden Indian policy reversals.

For global pricing, however, it creates a different reality.

India now possesses:

That makes India not just the world’s largest pulse consumer —

but increasingly the world’s most influential pulse price manager.

Final Thought

The significance of this policy is not merely about lower import duties.

It reflects a broader structural reality:

India is prioritizing supply security and inflation stability over short-term protectionism.

And in doing so, it is reshaping global pulse trade architecture for MY 2026/27 and beyond.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us