Falling Domestic Output Drives Turkey’s Pulse Imports to Near-Record Levels in 2025

07 February, 2026

Admin

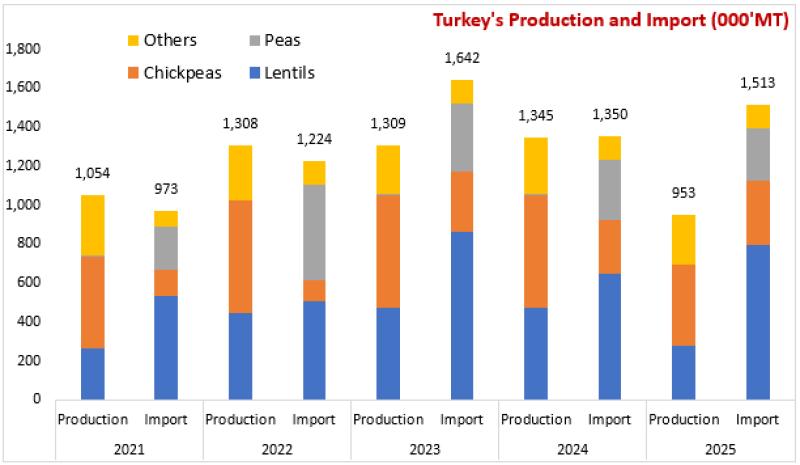

Turkey remains a major player in the global pulse market as a producer, importer, and exporter. However, Turkstat projections indicate a sharp contraction in domestic output in 2025. Chickpea production is expected to fall to 413 thousand metric tonnes (KMT), a decline of 28% compared with 2024. Lentil production is forecast at 280 KMT, representing a steep year-on-year drop of 41%.

Breaking lentils down by type, red lentil output in 2025 is estimated at 250 KMT, significantly lower than the 405 KMT recorded in 2024. Green lentil production is projected to fall to just 30 KMT, compared with 71 KMT in the previous year.

According to Turk Stat’s December 2025 trade statistics, Turkey’s total pulse imports for the January–December period reached 1,513 KMT, marking a 12% increase compared with the previous year. This volume represents Turkey’s second-highest pulse import level on record, surpassed only by imports in 2023, underscoring the impact of declining domestic production.

Russia emerged as Turkey’s largest pulse supplier in 2025, providing approximately 617 KMT of total imports. Kazakhstan followed as the second-largest supplier with 394 KMT, while Canada ranked third with 251 KMT, highlighting Turkey’s strong dependence on Black Sea and North American origins.

Lentils dominated Turkey’s pulse import profile, accounting for 53% of total pulse imports in 2025. Total lentil imports reached 795 KMT, rising significantly from 646 KMT in 2024 and representing the second-highest lentil import volume in Turkey’s history. Kazakhstan was the leading lentil supplier, shipping 387 KMT, followed by Canada with 223 KMT and Russia with 156 KMT.

Chickpea imports reached a new historical record in 2025, totalling 331 KMT, an 18% increase from the previous year. Russia was the dominant supplier, accounting for 222 KMT, while Mexico supplied 49 KMT and Canada contributed 17 KMT, reflecting a broader diversification of sourcing.

Pea imports, by contrast, declined in 2025, totalling 269 KMT, compared with 306 KMT in 2024. Despite the overall decrease, Russia maintained its position as the primary supplier, delivering approximately 239 KMT. Ukraine supplied 19 KMT, while Canada contributed a smaller volume of 5 KMT.

For more details on Pulses, Grains, and Oilseeds, subscribe to AgPulse Analytica.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us