The Desi Chickpea Equation: Why India Still Needs Imports Despite an 11 MMT Crop

09 June, 2026

Admin

The Indian chickpea market enters 2026/27 with what appears, at first glance, to be a comfortable supply situation.

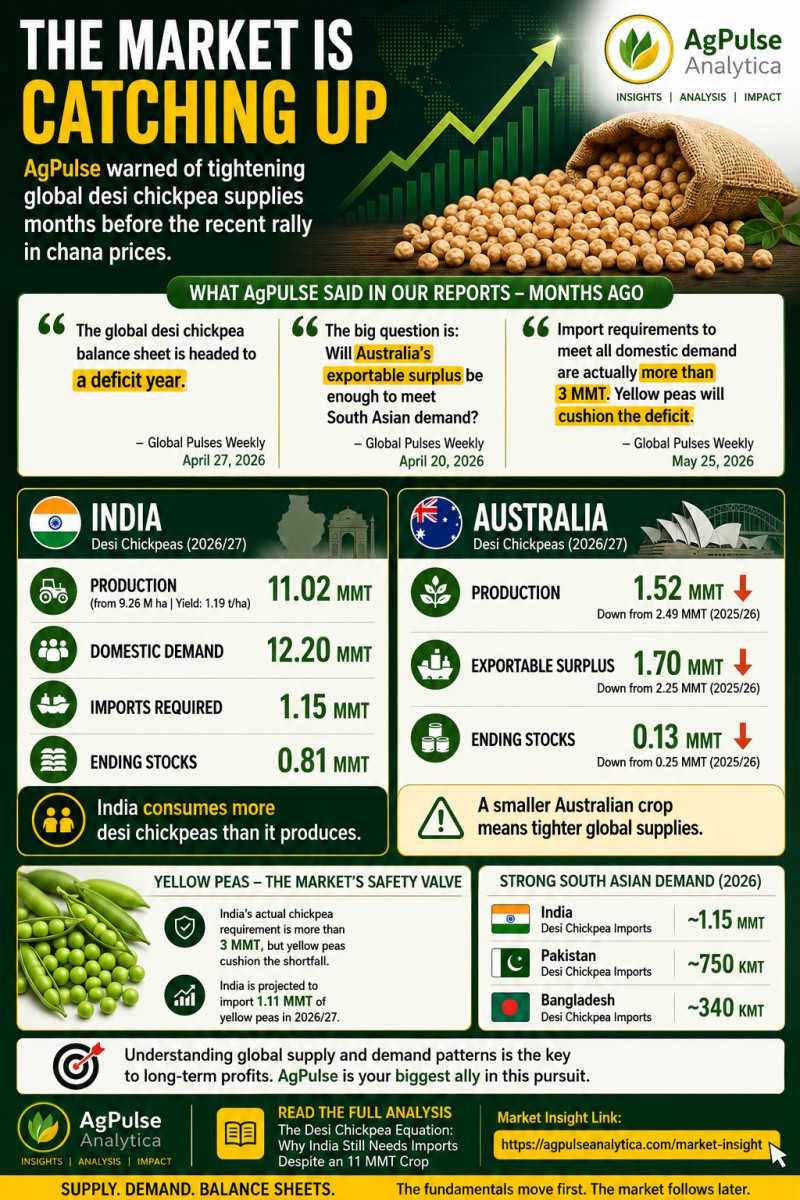

Domestic production has increased from 10.75 MMT in 2025/26 to an estimated 11.02 MMT in 2026/27, making it one of the largest desi chickpea harvests on record. Yet beneath this seemingly comfortable production figure lies a much tighter balance sheet than many market participants appreciate.

At AgPulse, our analysis suggests that India's desi chickpea market remains structurally dependent on imports, while the availability of exportable supplies from Australia—the world's dominant desi chickpea exporter—may be significantly lower than last year. The resulting gap is likely to be increasingly filled by yellow peas.

India's Production Is Large, But Demand Is Larger

For 2026/27, AgPulse estimates Indian desi chickpea production at 11.02 MMT from 9.26 million hectares harvested at an average yield of 1.19 tonnes per hectare.

While production is higher than the previous year's 10.75 MMT crop, domestic consumption is projected at 12.20 MMT.

This immediately highlights the core challenge facing the Indian market.

Even before considering stock rebuilding requirements, exports or procurement activity, domestic demand exceeds annual production by approximately 1.18 MMT.

This is not a one-year phenomenon. Chickpea consumption growth has consistently outpaced production growth, forcing India to remain a structural importer despite being the world's largest producer.

The Real Import Requirement Is Much Larger Than Official Import Numbers Suggest

One of the most misunderstood aspects of the chickpea market is the relationship between actual demand and reported import requirements.

AgPulse estimates India's 2026/27 desi chickpea balance sheet as follows:

At first glance, imports of approximately 1.15 MMT appear sufficient.

However, the balance sheet reveals a more nuanced reality.

To satisfy domestic consumption while maintaining comfortable stock levels, India would theoretically require more than 3 MMT of additional supplies. The reason imports remain projected near 1.1 MMT rather than 3 MMT is the presence of two critical buffers:

In other words, the market is not being balanced exclusively by chickpeas.

It is being balanced by a broader pulse complex.

Government Stocks Have Become a Key Market Variable

The role of government agencies has become increasingly important.

Large procurement programs have transferred significant quantities of chickpeas from commercial channels into government inventories.

These stocks still exist physically, but their impact on market availability depends entirely upon the timing and volume of future releases.

This is why import requirements cannot be viewed in isolation.

If government agencies release stocks aggressively, import demand can decline.

If stocks remain largely locked away, private trade will need greater import volumes to bridge the gap.

The government's stock management strategy therefore remains one of the most important variables in the Indian chickpea balance sheet.

Australia Is the Critical Supplier

For the global desi chickpea market, Australia remains the most important source of exportable surplus.

AgPulse estimates Australian production at 1.52 MMT for 2026/27, down sharply from 2.49 MMT the previous season.

The reduction is driven primarily by yield risk rather than acreage.

While acreage is still expected to exceed one million hectares, dry planting conditions across Queensland and New South Wales create the possibility of significant yield variability.

Under AgPulse's realistic scenario:

The consequence is straightforward.

Australia's exportable surplus declines by approximately 550 KMT year-on-year.

For a market heavily dependent on Australian supplies, this is a significant reduction.

Can Australia Meet South Asian Demand?

This is the central question for the coming season.

Australia's projected export surplus of 1.70 MMT must satisfy demand from multiple destinations, including:

At the same time, demand across South Asia remains elevated.

Pakistan is projected to import approximately 750 KMT of desi chickpeas during 2026.

Bangladesh imports are projected near 340 KMT.

Together, Pakistan and Bangladesh alone account for more than 1 MMT of import demand.

When India's projected requirement of around 1.15 MMT is added, total South Asian demand comfortably exceeds Australia's projected exportable surplus.

This explains why Australian production outcomes have become the most important variable in the global desi chickpea market.

A crop close to last year's 2.5 MMT would create a relatively comfortable situation.

A crop near 1.5 MMT creates a much tighter market.

Tanzania Provides Support, But Not a Solution

Tanzania continues to expand its role within the Indian import program.

AgPulse projects Tanzanian production at 230 KMT and exports at approximately 198 KMT in 2026/27.

The favourable tariff treatment available to Tanzanian chickpeas has made the origin increasingly attractive to Indian buyers.

However, Tanzania remains a supplementary supplier rather than a replacement for Australia.

Even if every tonne of Tanzanian exports were directed toward India, it would cover only a small portion of India's overall import requirement.

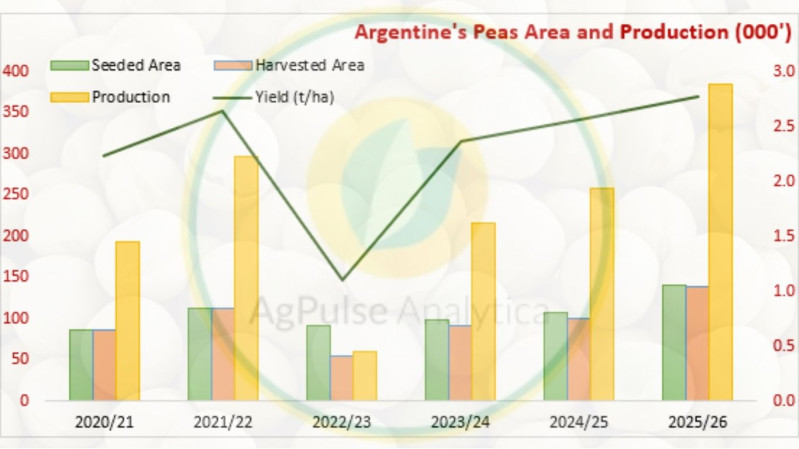

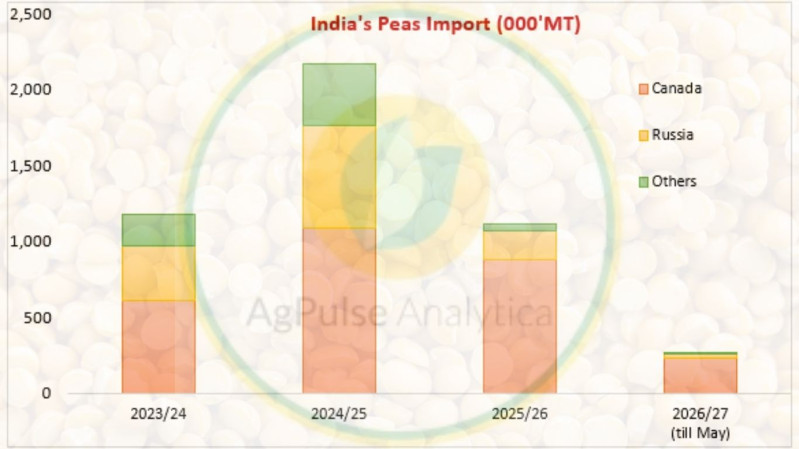

Yellow Peas Are Becoming India's Safety Valve

The most important balancing mechanism in the market may not be chickpeas at all.

It may be yellow peas.

AgPulse has repeatedly highlighted that India's chickpea deficit is being partially offset through pea imports.

The logic is straightforward.

When chickpea supplies tighten and prices rise relative to peas, substitution becomes increasingly attractive.

Importers, processors and consumers gain access to a larger global supply pool through peas than through desi chickpeas.

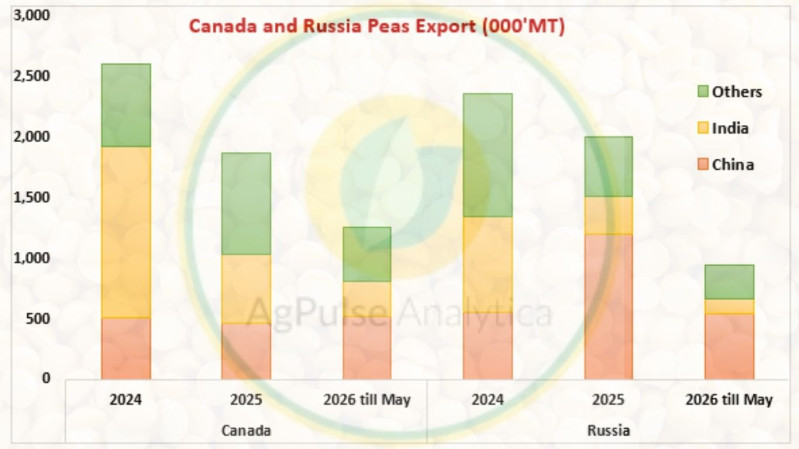

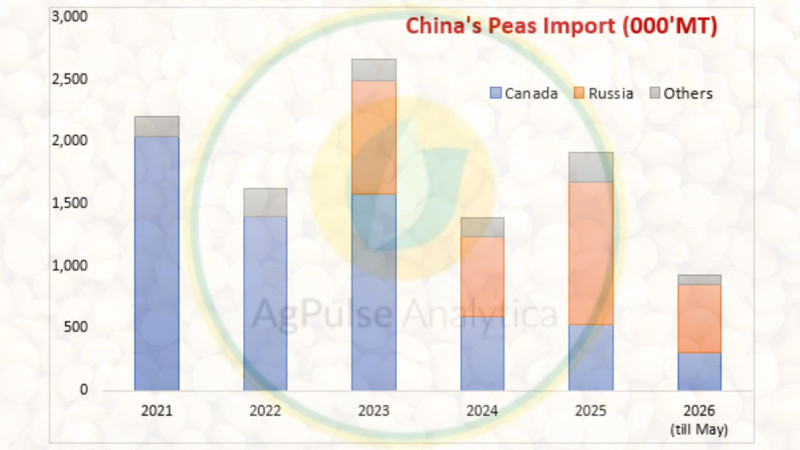

The global pea balance sheet remains considerably more comfortable than the desi chickpea balance sheet.

Large inventories remain available in Canada, Russia and other exporting nations.

As a result, yellow peas effectively act as a pressure-release valve for the Indian pulse market.

Without this substitution mechanism, India's chickpea import requirement would be substantially larger than current projections.

AgPulse Take

The 2026/27 season is not defined by a shortage of Indian chickpea production.

An 11 MMT crop is historically large.

Instead, the market is defined by a mismatch between domestic production and domestic consumption.

India consumes more desi chickpeas than it produces and therefore remains dependent upon imports.

The challenge becomes more significant because Australia's exportable surplus is projected to decline sharply from last year, limiting the quantity available to South Asian buyers.

Government-held stocks and yellow pea imports therefore become critical balancing factors.

In practical terms, the Indian chickpea market is no longer being balanced solely by chickpeas.

It is being balanced by three interconnected pillars:

Any disruption to one of these pillars increases the importance of the other two.

That is why the outlook for Australian production and the pace of yellow pea imports may ultimately matter just as much as the size of India's own chickpea crop.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us