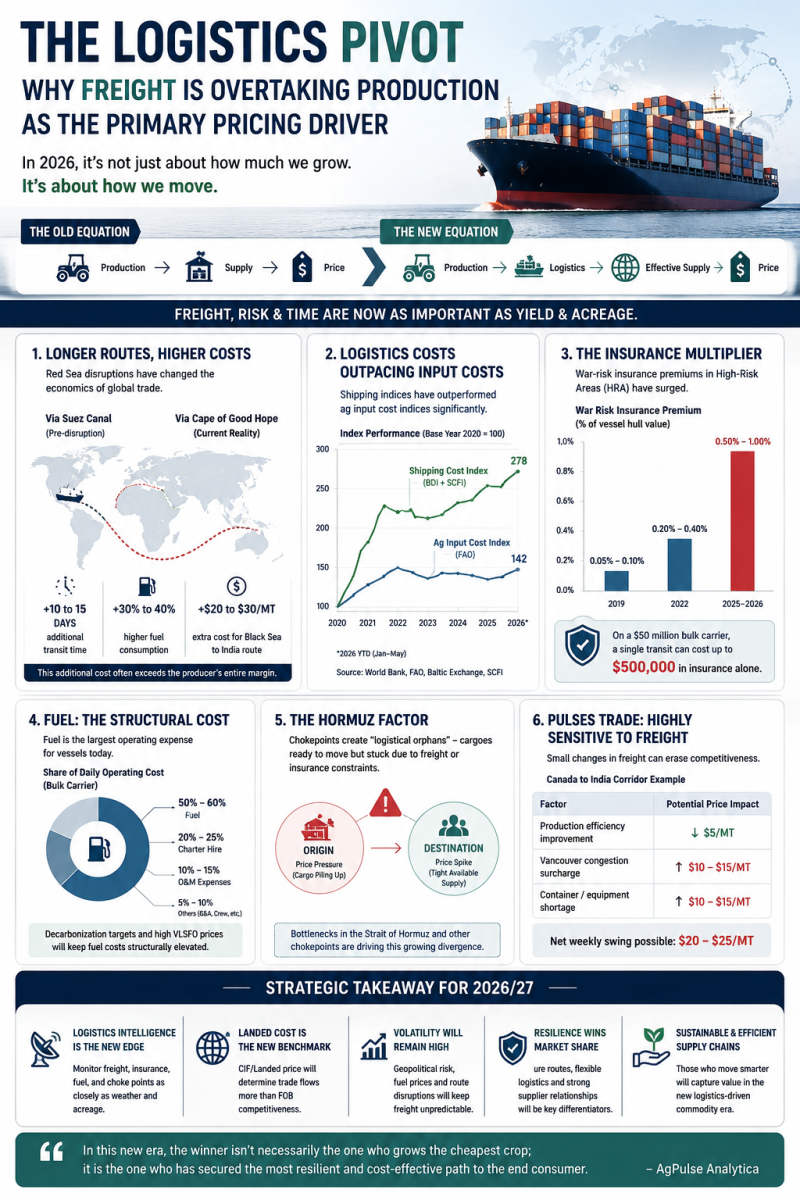

The Logistics Pivot: Why Freight is Overtaking Production as the Primary Pricing Driver in Global Agri-Commodity Markets

12 May, 2026

Admin

For decades, global agricultural commodity markets were primarily driven by production fundamentals — acreage, weather, fertilizer costs, and yield expectations. Supply determined price, and traders focused intensely on the farm gate.

That framework is undergoing a structural shift in 2026. Logistics and freight costs have become increasingly volatile and, in many cases, more decisive than production itself. The market is transitioning from a purely production-centric model to a logistics-centric one.

The Decline of Pure FOB Pricing

Historically, trade revolved around FOB (Free on Board) pricing. Once cargo was loaded at origin, freight was often treated as a secondary, pass-through cost. Today, buyers are laser-focused on CIF (Cost, Insurance, and Freight) and total landed costs.

Geopolitical disruptions have introduced large risk premiums into global shipping. The prolonged Red Sea and Suez Canal crisis is a prime example. Rerouting around the Cape of Good Hope has added 10–14 days to voyage times and increased fuel consumption by 30–40%. For bulk carriers shipping yellow peas or other pulses from the Black Sea to South Asia, this has translated into additional freight costs of $20–35 per MT — often wiping out producer margins.

A cargo that looks attractive on FOB terms can quickly become uncompetitive once freight, insurance, and delay risks are factored in.

The Rise of “Effective Supply”

Modern markets increasingly operate on the concept of “effective supply” rather than physical production. A country can harvest a record crop, but if freight rates spike, vessels are unavailable, or routes become too risky, a significant portion of that supply effectively disappears from the global market.

This distinction is particularly critical in the pulses sector, where margins are thin and buyers are highly price-sensitive to landed costs.

When Logistics Outweigh Input Costs

Recent developments highlight how logistics are overshadowing traditional agronomic variables:

- Insurance Costs: War-risk premiums in High-Risk Areas have risen sharply. In volatile corridors, premiums can reach 0.5–1.0% of hull value, adding hundreds of thousands of dollars per voyage for large bulk carriers.

- Fuel Economics: IMO decarbonization rules and the shift to Very Low Sulfur Fuel Oil (VLSFO) have structurally increased vessel operating expenses, with fuel now accounting for 50–60% of daily costs.

- The Hormuz Factor: Ongoing tensions in the Strait of Hormuz have created additional bottlenecks for fertilizer and agricultural cargoes, producing “logistical orphans” — commodities available at origin but uneconomical to move.

The result is a paradoxical market: localized price weakness at export origins alongside price spikes at destination markets.

Pulses Markets: Especially Vulnerable

Pulses are particularly exposed due to fragmented trade flows and thin margins. While a $10/MT change in fertilizer costs may have limited impact, a $30–40/MT swing in freight can completely alter export competitiveness.

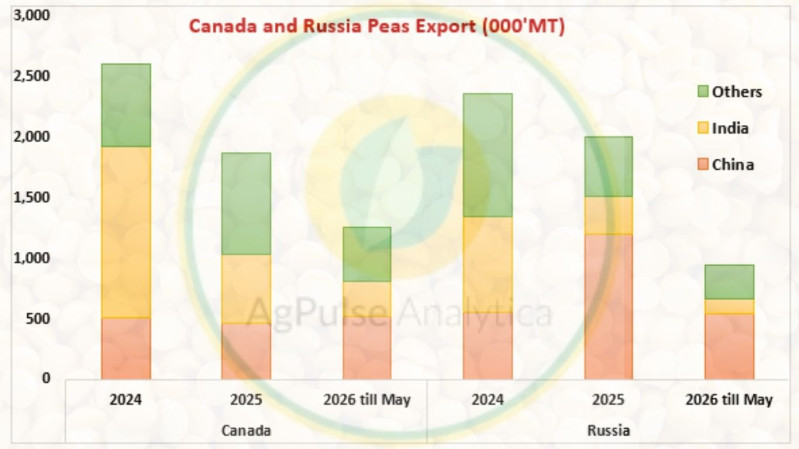

In the Canada–India corridor, for instance, port congestion surcharges or container shortages can swing delivered prices by $20–25/MT within days — far outweighing incremental gains in farm-level efficiency.

Strategic Implications for 2026/27

For commodity professionals, monitoring logistics has become as critical as tracking weather and acreage reports. Key indicators now include:

- Baltic Dry Index (BDI)

- Shanghai Containerized Freight Index (SCFI)

- Bunker fuel spreads

- Vessel availability

- Insurance premiums

- Geopolitical chokepoints

At AgPulse Analytica, we view logistics intelligence as equally important as agronomic intelligence when forecasting price direction.

In the new market reality, the winners will not only be those who produce efficiently — but those who can secure resilient, cost-effective, and reliable routes to the end consumer.

Freight is no longer just a cost. It has become a core competitive advantage.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us