Why Yellow Peas are becoming India’s "Strategic Reserve" in the Pulse Market

08 May, 2026

Admin

As we move into MY 2026/27, the Indian pulse landscape is facing a significant structural gap. Despite a domestic chickpea crop currently under harvest with prices hovering near MSP, the math points to a clear deficit that global markets must fill.

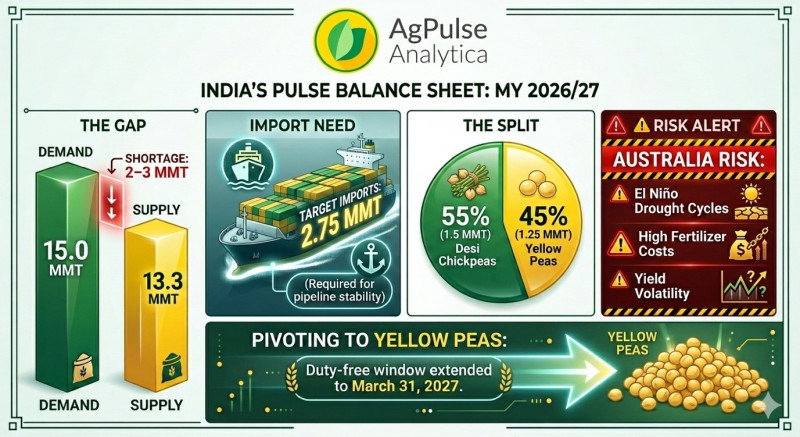

The Supply-Demand Reality:When viewing peas and chickpeas as a combined supply pool, India is currently facing a 2–3 MMT shortage.

· Total Consumption:Nearly 15 MMT.

· Domestic Supply (Production + Carry-in):13.3 MMT.

· The Gap:India will require a minimum of 2.75 MMT in imports to meet domestic use and maintain essential pipeline stocks.

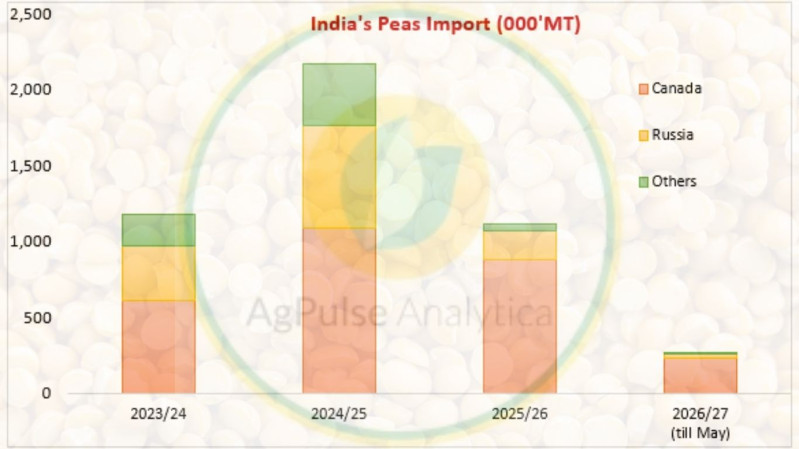

The "Yellow Pea" Pivot:The government has proactively extended the pea import policy for an additional year, keeping doors open for the entirety of MY 2026/27. While the current target is a split of 1.5 MMT in desi chickpeas and 1.25 MMT in yellow peas, external factors are shifting the trade toward the latter.

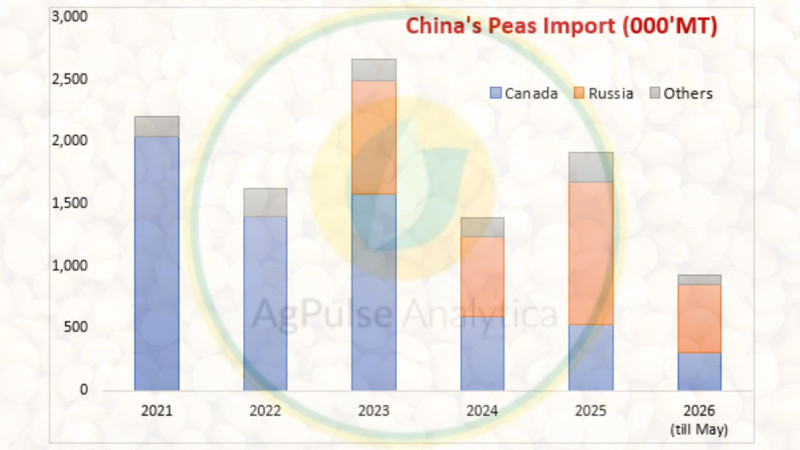

The Australia Risk Factor:High fertilizer costs, low soil moisture, and the looming El Niño in Australia threaten their 2026 crop. If Australian desi chickpea supplies fall short of the 1.5 MMT target, Indian trade will likely pivot even more heavily toward yellow peas, where global supplies are diverse and abundant.

The Bottom Line:Expect the price spread between desi chickpeas and yellow peas to widen in South Asia, pushing more volume toward yellow pea imports as the most reliable hedge against regional supply shocks.

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us