Wheat-A Bottomless Pit

23 March, 2023

Admin

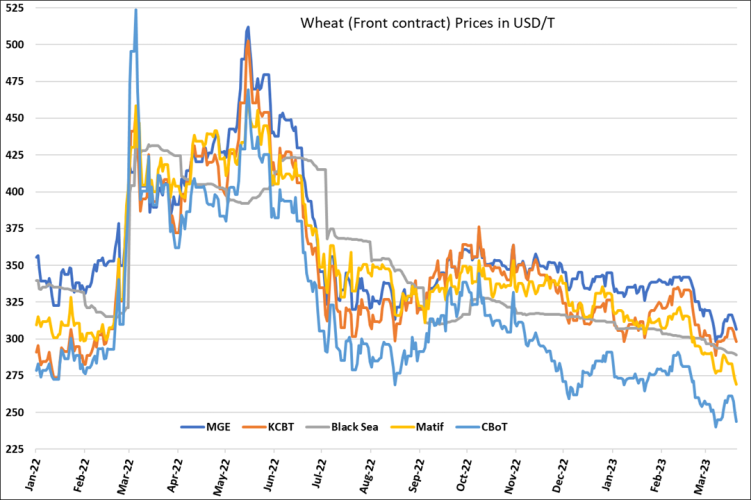

At a time, when the stocks to use ratio of world wheat is hovering near multi years’ lows, the prices are relentlessly moving down. Not just at the global level, inventories are tight at all major exporters except Russia and Australia. The demand bloc, which we call all countries except major exporters, China and India, is also facing lowest inventory levels, compared to their domestic use in more than a decade.

With such low stocks, why are the wheat benchmark prices across globe are continuously falling? Chicago front contract is trading below $250/T, Black Sea physical is trading below $300/T for 12.5% protein and Matif wheat front contract is now below $275/T.

Continuous flow from Russia, Australia and Canada and possibility of an increase in shipment pace from USA in Q4 are keeping the physical markets under stress. The constantly burgeoning short fund position in major derivative exchanges is also fueling the bear run.

How long can that continue? We do not except the bear run to continue for long, given the depleting inventory levels in multiple geographies. Once the tide turns, many of the importers, which have low forward coverage will come back to book their requirements. Any adverse weather event in any of the major producers in the next four months can also trigger the end of downturn.

For more such info, subscribe to our weekly analytical reports for only USD150 per month at https://agpulseanalytica.com/subscribe/international

Subscribe to Supporting Agribusiness Leaders Find Market Insights for Smart Growth

![]()

Global Intelligence for Pulses, Grains & Oilseeds

Empowering informed decisions across the agricultural value chain with timely market insights, forecasting models, and trade analysis.

Follow Us